Indobell Insulations Gains 5% After Securing Key US Export Order; Stock Hits Upper Circuit

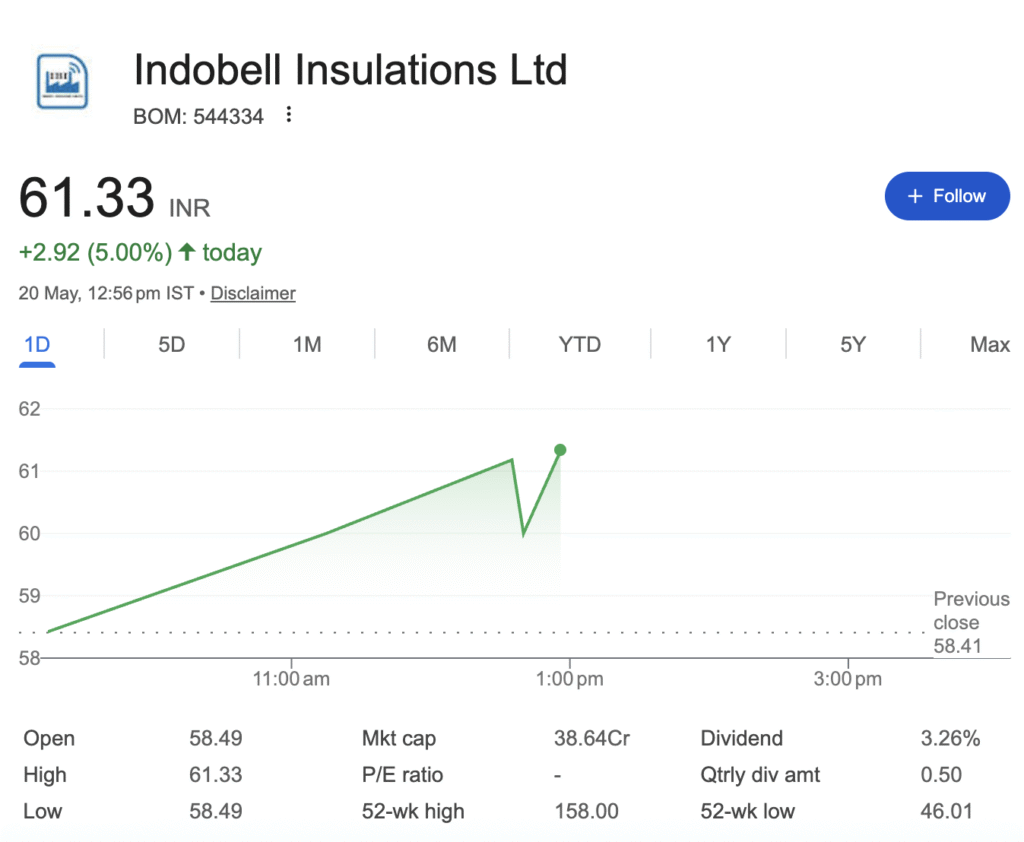

Mumbai, May 20 — Shares of Indobell Insulations Limited (BOM: 544334) rallied 5% to hit the upper circuit at ₹61.33 in Wednesday’s trade after the company announced a significant export order from US-based energy infrastructure major GE Vernova Operations LLC.

The micro-cap insulation specialist informed the exchanges that it has secured a contract to supply Steam Turbine Insulation – Blanket Therm valued at USD 91,300 (approx. ₹76.5 lakh). The order is scheduled for execution by January 2027 under FCA (Free Carrier) Incoterms, with payment terms set at Net 150 Monthly.

Cumulatively, the GE Vernova orders alone touch roughly $1.24 million. For a firm of this size, that’s serious business.

The company has also secured domestic orders:

- NTPC: ₹85.15 lakh ($102,000) in March 2026 for gas turbine re-insulation.

- Goa Shipyard (via GeM): ₹1.47 crore ($176,500) in April 2026 for defence frigate insulation, due by September 2026.

Total known order inflow since January 2026: roughly $1.5 million (₹12.5 crore) – representing nearly 50% of its FY25 revenue.

COMPANY OVERVIEW

Indobell is both a manufacturer and contractor of insulation products. Its core offerings include:

- Ceramic & Mineral Fibre Nodules – Used in brake blocks, heat shields, industrial equipment

- Granulated Rockwool & Spray Insulation – Thermal and acoustic insulation

- Prefabricated Thermal Insulation Jackets – Energy conservation, safety, process equipment insulation

- LRB Mattress & Ceramic Fibre Blanket Insulation

- Fibreglass Aerogel Insulation

Beyond products, the company provides consultancy, engineering, fabrication, installation, project management, and global logistics services.

Industries served include power plants, railways, aeronautics, navigation, commercial buildings, and industrial plants. Exports reach Bangladesh, Germany, Taiwan, Poland, South Korea, and the United States. Notably, Indobell and one other company are reportedly the only two players in India with the technology to produce ceramic fibre nodules for high-temperature applications – a structural moat.

Key manufacturing units are located in West Bengal and Maharashtra.

FINANCIAL ANALYSIS

Revenue & Profit Trends

| Parameter | FY2025 | FY2024 | FY2023 | FY2022 | TTM (Sep 2025) |

|---|---|---|---|---|---|

| Operating Revenue (₹ Cr) | 25.73 | 17.88 | 20.77 | 9.61 | 27.19 |

| Revenue Growth (YoY) | +43.89% | -13.89% | +116.10% | — | — |

| Gross Profit (₹ Cr) | 10.73 | 7.59 | 6.71 | 4.90 | 10.89 |

| Net Profit (₹ Cr) | 2.19 | 1.03 | 0.90 | 0.15 | 2.24 |

| Net Profit Growth (YoY) | +111.69% | +14.72% | +486.77% | — | — |

| Operating Profit Margin (OPM) | 11.20% | 11.67% | 9.00% | 8.64% | 5.26% |

| EPS (Basic, ₹) | 3.47 | 2.52 | 13.19 | 2.20 | 3.02 |

Key Takeaway: Revenue jumped 44% in FY2025, while net profit more than doubled – growing 112% year-on-year. However, Q2 and Q3 of 2025 saw a dip in operating margins due to seasonal or project-specific factors, which investors should monitor in upcoming results.

Margins & Operational Efficiency

| Parameter | FY2025 |

|---|---|

| EBITDA Margin | ~11-12% (core operations) |

| Net Profit Margin | 8.50% |

| Return on Equity (ROE) | 20.69% |

| Return on Capital Employed (ROCE) | 23.70% |

The company has been maintaining a healthy dividend payout of ~28-30%, with a current dividend yield of approximately 3.21% – a rare combination for a micro-cap industrial firm.

Balance Sheet Health

| Parameter | Current (May 2026) | FY2025 | FY2024 |

|---|---|---|---|

| Debt/Equity Ratio | 0.04 | 0.16 | 0.93 |

| Net Debt/Equity | -0.19 | 0.04 | 0.78 |

| Current Ratio | 9.86 | 2.21 | 1.34 |

| Quick Ratio | 5.25 | 1.81 | 0.94 |

| Book Value per Share (₹) | ~25.30 | 25.30 | ~9.00 |

Key Takeaway: Debt/equity has collapsed from 0.93 in FY2024 to just 0.04 in FY2025 – the company is virtually debt-free. Current ratio has improved from 1.34 to 9.86, and quick ratio from 0.94 to 5.25, signalling excellent short-term liquidity.

However, cash flow remains a concern: operating cash flow turned negative in certain periods, and debtor days have increased from 72 days to 141 days, raising questions about working capital efficiency.

Upcoming Catalyst

The Board of Directors is scheduled to meet on May 22, 2026, to consider and approve the financial results for the quarter/year ended March 31, 2026 – a potential price trigger.

RISK FACTORS THAT CANNOT BE IGNORED

- Tiny order book relative to market cap: Even $1.5 million in orders is small for a listed entity. This is a sentiment-driven micro-cap, not a revenue powerhouse.

- Long execution timelines: The latest GE Vernova order extends into June 2027 – over 12 months away. Revenue recognition is back-ended.

- Weak cash flow from operations: FY25 saw negative operating cash flow of -₹4.32 crore despite a net profit of ₹2.19 crore – a red flag.

- Working capital pressures: Receivables ballooned from ₹6.59 crore in FY24 to ₹14.23 crore in FY25 – over 55% of annual sales locked in debtors.

- Low institutional interest: Zero FII holding and minimal DII holding suggest larger funds are staying away. Retail dominance increases volatility.

- Price volatility is real: The stock has swung from ₹46 to ₹158 in the last 12 months – a 243% range. This is not for the faint-hearted.

GROWTH CATALYSTS TO WATCH

✅ GE Vernova as a repeat customer: The US energy giant has placed 5+ separate orders since March 2026 – a strong vote of confidence. Repeat business is likely.

✅ Defence sector entry: The Goa Shipyard order for Frigates Project Yar d1258-59 opens the door to more defence contracts.

✅ Tailwinds from energy efficiency: The Indian mineral wool insulation market is projected to grow at a CAGR of 6.44% through FY2033, while India’s overall insulation market is expected to reach $3.94 billion by 2034 (CAGR 3.93%).

✅ Export credibility: Supplying GE Vernova enhances quality certifications and global standing, potentially unlocking more US/EU opportunities.

✅ Zero debt & strong liquidity: Net debt/equity of just 0.04 puts the company in a strong position to fund growth without raising fresh capital.

THE BOTTOM LINE

| Aspect | Rating | Remarks |

|---|---|---|

| Financial Health | ⭐⭐⭐⭐ | Debt-free, strong ROE, improving margins |

| Growth Trajectory | ⭐⭐⭐ | Orders are promising but small |

| Valuation | ⭐⭐⭐½ | Undemanding at 21x P/E given 44% revenue growth |

| Institutional Confidence | ⭐⭐ | Zero FII holding is a concern |

| Liquidity & Trading | ⭐⭐ | Micro-cap; prone to sharp moves |

| Risk Profile | 🔴 HIGH | Negative operating cash flow, delayed revenue, retail-dominated |

Relative Positioning

At ₹62 per share, the stock trades 60% below its 52-week high of ₹158 – but at 17.5x P/E, it’s not demanding given 44% revenue growth and 112% profit growth in FY2025.

However, valuation is not the primary concern here. The bigger questions revolve around:

- Cash flow sustainability

- Working capital management

- Ability to convert order book into consistent profitability

FINAL TAKE

Indobell Insulations presents a classic micro-cap paradox.

On the positive side: Zero debt, 20%+ ROE/ROCE, a 3.2% dividend yield, a blue-chip global customer (GE Vernova) placing repeat orders, and a unique product position in a niche market.

On the flip side: Negative operating cash flow, ballooning receivables, micro-cap volatility, and heavy dependence on a single export client.

The company’s fundamentals are improving – revenue up 44%, profit up 112%, and debt nearly eliminated. But cash flow and working capital efficiency remain unresolved questions.

For those seeking deep-dive industrial stories with transformation potential, Indobell warrants a place on the watchlist. For those focused on cash-conversion consistency and institutional validation, the “wait and watch” approach until the cash flow picture clarifies may be more prudent.

Upcoming catalyst: The May 22 board meeting and FY26 results will be pivotal in determining whether the operational story is finally translating into reliable cash generation – or if the working capital pressures continue to weigh.

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Investors are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.