Yaan Enterprises Share Price Hits 52-Week High After Blockbuster Order: Can this Small-Cap Sustain the Rally?

A Rs. 7.30 Crore domestic supply contract with a state cooperative society fuels investor optimism, propelling shares to new highs.

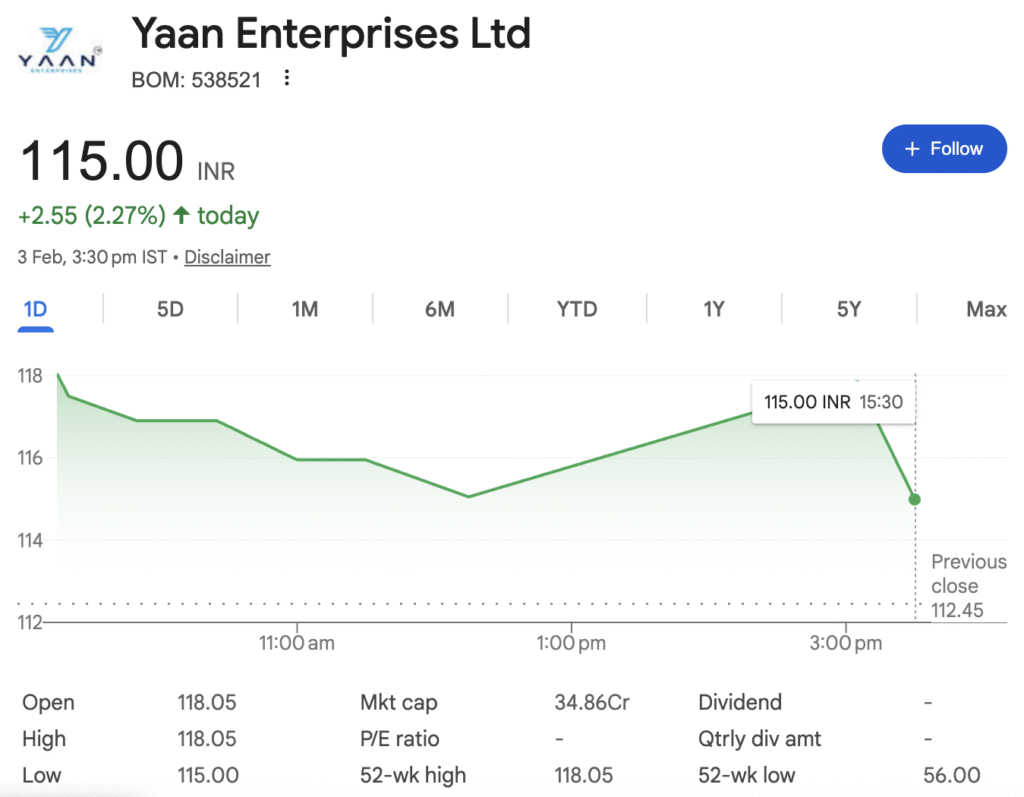

Mumbai, February 4, 2026 – Shares of Yaan Enterprises Limited (BSE: 538521) witnessed a significant surge in early trading yesterday, hitting a fresh 52-week high of ₹118.05, after the company announced the receipt of a substantial purchase order.

In a regulatory filing to the BSE, the agri-commodity focused company informed that it has secured a purchase order from the State Agri Horticultural Development Co-operative Society Limited, Thiruvananthapuram, for the supply of yellow maize. The order is valued at approximately Rs. 7.30 Crores, marking a significant deal for the small-cap firm, which currently commands a market capitalization of around ₹34.86 Crores.

Details of the Deal:

According to the disclosure made under SEBI’s Listing Obligations and Disclosure Requirements (LODR), the key terms of the contract include:

- Goods: Supply of Yellow Maize (Order Ref: SAHS/YAAN/125/2025-26)

- Counterparty: A domestic government-linked cooperative society.

- Execution Timeline: The order is to be fulfilled within 1-2 months, indicating near-term revenue recognition.

- Payment Terms: 25% advance payment, with the balance payable upon completion of supply and receipt of a quality analysis certificate.

The Catalyst: Explosive Growth and a Major Order

The immediate trigger for the market’s excitement is two-fold. First, the company’s standalone financial results for the quarter ended December 2025 reveal nothing short of a transformation. Sales skyrocketed by 416.28% to ₹8.88 crore, while net profit rose by a solid 84.21% to ₹0.35 crore.

Second, hot on the heels of these results, the company announced it received a purchase order from the State Agri Horticultural Development Co-operative Society Limited for the supply of yellow maize, valued at approximately ₹7.30 Crores (or ₹73 million). For a company with a market capitalization of around ₹34.86 Crore, an order representing over 20% of its total market value is a materially significant event.

But the core investment debate centers on whether Yaan is embarking on a sustainable, scalable growth path or remains a volatile small-cap susceptible to execution risks and valuation gravity. This report dissects its financial health, competitive moat, and the viability of its growth triggers to determine its suitability for different investor profiles.

1. Business Overview

Company Background & History: Incorporated in 1989, Yaan Enterprises has operated under the radar for decades. Formerly known as Crown Tours Ltd, its journey reflects a constant strategic evolution from a pure-play tour operator to its current multi-segment structure.

Core Business Segments & Revenue Contribution: The company operates a highly diversified portfolio with five distinct segments. Precise revenue breakdowns by segment are not publicly disclosed, making it difficult to assess the profitability of each vertical. The segments are:

- Infrastructure & Works Contract: Expertise in tunneling, roads, and highways. Notably, it has undertaken work under the PM Kusum project.

- Tourism (Yaantrip): Operates a one-stop online platform covering B2C, B2B, and B2E travel needs.

- Green Energy: Undertakes projects in desalination, solar, and wind energy segments.

- Gems & Jewelry: Involved in the export, import, and processing of precious metals like gold and platinum.

- Export, Trading & Agri-Supply: Specializes in logistics for high-value products (crude, gold, pesticides) and, as recent orders show, has pivoted into bulk agri-commodity trading like yellow maize.

Presence: The company’s operations are primarily domestic. Recent major orders, such as the ₹6.5 crore and ₹8 crore yellow maize supply contracts, have been from domestic state cooperative societies.

Business Model: In simple terms, Yaan Enterprises functions as a project-based and trading conglomerate at a small scale. It does not own large fixed assets or brands but acts as an intermediary and executor. It secures contracts (for construction, supply, or travel services) and fulfills them by managing operations and logistics. The recent agri-supply orders highlight a trading model where it likely sources commodities to fulfill specific institutional demand.

2. Industry & Sector Analysis

Yaan’s diverse play exposes it to multiple, non-correlated industries. The recent focus on agri-supply places it in the large and steady Indian animal feed market, where yellow maize is a key input driven by consistent demand from poultry and dairy industries. Its infrastructure segment benefits from the government’s continued push for capital expenditure, with the 2026 Union Budget proposing an increase in public capex to ₹12.2 lakh crores. The tourism segment stands to gain from budget measures like lowering TCS on overseas tour packages and promoting niche tourism.

Competitive Intensity (Simplified):

- Rivalry: Extremely High. Each segment is crowded with established players and traders.

- Supplier Power: High. As a small trader and contractor, Yaan has limited bargaining power against suppliers or equipment providers.

- Buyer Power: High. Clients, especially government bodies, seek competitive bids, squeezing margins.

- Threat of New Entry: High. Low barriers to entry in trading and small-scale contracting.

- Threat of Substitutes: Medium. Services are often commoditized.

Industry Cycle Positioning: The company is attempting to position itself in early-cycle recovery sectors. The anticipated business cycle turnaround in 2026, supported by fiscal stimulus and monetary easing, could benefit its infrastructure and domestic trade segments if execution is flawless.

3. Financial Performance Deep Dive (5-Year Analysis)

A five-year review shows a company recovering from a low base but struggling with profitability consistency and quality of earnings.

Table: Key Financial Metrics (Figures in ₹ Crore, except per-share data)

| Financial Metric | FY 2025 | FY 2024 | FY 2023 | FY 2022 | FY 2021 | 5-Yr Trend |

|---|---|---|---|---|---|---|

| Revenue from Operations | 5.41 | 4.98 | 2.45 | 1.21 | 1.91 | Volatile; Recent Growth |

| EBITDA Margin | 8.3% | 14.1% | 3.7% | -9.9% | -19.4% | Highly Erratic |

| PAT Margin | 8.5% | 9.8% | 2.4% | -19.0% | -173.8% | Improved but Unstable |

| Return on Equity (ROE) | 10.6% | N/A | N/A | N/A | N/A | Improved from lows |

| Return on Capital Employed (ROCE) | 8.77% | N/A | N/A | N/A | N/A | Below Cost of Capital |

| Debt-to-Equity | Low (~0.1) | Low | Low | Low | Low | Conservatively Financed |

| Operating Cash Flow | Negative | Negative | Positive | Positive | Negative | Weak & Unpredictable |

| EPS (₹) | 1.48 | 1.58 | 0.20 | -0.75 | -10.71 | Recovered from extreme loss |

Quality of Earnings & Margin Analysis: The financials raise several concerns. The EBITDA margin contracted sharply from 14.1% in FY24 to 8.3% in FY25, despite revenue growth. This indicates an inability to convert top-line growth into operating leverage, likely due to rising costs or competitive pricing in new contracts. Operating Cash Flow has been persistently weak or negative, suggesting earnings are not being realized as cash—a critical red flag often stemming from a stretched working capital cycle or inventory buildup.

Red Flags:

- Inconsistent Profitability: Wild swings in margins and profits point to a lack of a stable, scalable business model.

- Weak Cash Generation: Consistent negative operating cash flow questions the sustainability and quality of reported profits.

- Low Return Ratios: An ROCE of 8.77% is below what would be considered a healthy return for the risks of a small-cap business.

4. Balance Sheet & Cash Flow Analysis

Debt Structure & Working Capital: The balance sheet is not leveraged, with minimal debt. This is a positive, providing a margin of safety. However, a major concern is the ballooning of debtor days from 57.7 to 85.7 days, indicating slower collections from customers and inefficient working capital management. This directly explains the poor operating cash flows.

Capex vs. Cash Generation & Free Cash Flow: The company has not been engaged in significant capital expenditure, as seen from minimal fixed assets. The business is not free cash flow generative, as operational cash inflows are insufficient. It funds its operations and working capital needs through internal accruals and potentially advances from customers (as seen in the 25% advance payment in recent maize orders).

5. Decoding the Promoter Holding Pattern

- High and Increasing Stake Signals Confidence: A promoter stake of nearly 69% is significantly high, indicating strong insider control and, typically, confidence in the company’s future. The steady increase from ~64.6% over the past two years is particularly noteworthy. This upward trend often signals promoters’ belief in the company’s strategic direction and growth prospects, especially during its recent pivot towards infrastructure, agri-supply, and other diversified segments.

- Zero Pledging is a Major Positive: One of the strongest governance positives for Yaan Enterprises is that 0.0% of the promoter shares are pledged. Share pledging is often viewed as a red flag because it introduces financial risk; if share prices fall, promoters may face margin calls, potentially leading to forced sales and stock price volatility. The absence of pledging eliminates this risk and indicates the promoters are not using their holdings for personal leverage, adding a layer of financial stability.

- Complete Absence of Institutional Investors: The data shows 0% holding by Foreign Institutional Investors (FIIs), Domestic Institutional Investors (DIIs), mutual funds, or insurance companies. While this means the stock lacks the validation and stability that institutional backing often provides, it also presents a potential future catalyst. Should the company’s new business segments (like the recent large maize supply orders) demonstrate consistent execution and profitability, it could attract institutional interest, leading to significant re-rating.

⚖️ Implications for Retail Investors

From a governance and sentiment perspective, the promoter holding pattern is a clear positive. High, increasing, and unencumbered promoter ownership aligns their interests directly with minority shareholders. However, as highlighted in the previous deep-dive analysis, this must be weighed against fundamental concerns like inconsistent profitability, weak cash flows, and a premium valuation.

For you as an investor, this promoter analysis refines the overall thesis:

- The Bull Case is Supported: Promoters are “putting their money where their mouth is,” backing their diversification strategy with increased ownership.

- A Key Monitorable: The next major move to watch would be any sign of institutional investors (FII/DII) initiating a stake, which would be a strong external validation of the business turnaround.

6. Competitive Positioning & Moat

Yaan Enterprises operates in highly competitive fields with virtually no economic moat.

- Market Share & Pricing Power: It holds negligible market share in any segment and has no pricing power, competing on cost and relationships.

- Entry Barriers & Switching Costs: Barriers are low in trading and small-ticket contracting. Customer switching costs are negligible.

- Brand Strength & Scalability: The “Yaan” brand carries little weight. The scalability of its current project-based model is highly questionable, as scaling requires significantly more working capital and operational bandwidth, which its cash flows cannot support.

7. Growth Triggers & Future Outlook (2-3 Years)

- Order Book Execution: The successful execution of the ₹14.5+ crore agri-order pipeline is the most immediate trigger. Timely completion and profit realization are crucial.

- Segment Rationalization: The market would reward a strategic focus on 1-2 high-potential segments (e.g., agri-trading linked to government schemes, niche infrastructure) over the current scattered approach.

- Margin Improvement: Leveraging the newly announced ₹10,000 crore SME Growth Fund from the 2026 Budget could provide cheaper working capital, potentially easing the debtor cycle and improving margins.

- Industry Tailwinds: Government focus on agriculture (e.g., integration of AI tools) and infrastructure spending provides a conducive environment, if the company can position itself correctly.

Long-term Visibility: Currently, visibility is very low. Beyond the announced orders, there is no clear roadmap or large-capacity expansion plan to drive multi-year growth.

8. Valuation Analysis

Yaan Enterprises trades at valuations that are difficult to justify based on fundamentals.

- Current Multiples: P/E of 57.7 and Price-to-Book of 7.79.

- Peer Comparison & Historical Average: It trades at a significant premium to typical “fundamentally strong” small-caps, which are often screened for P/E < 25, low debt, and high ROCE. Its own historical P/E has been volatile due to erratic earnings.

- Valuation Justification: The current valuation is not supported by its financial performance (low ROCE, unstable margins) or growth visibility. It appears to be expensive, pricing in overly optimistic success from the new diversification into agri-trading, while ignoring the core financial weaknesses and lack of moat.

9. Risk Factors (Very Important)

- Execution Risk (HIGH): Failure to execute new orders profitably or on time is the single biggest risk.

- Financial Risk (HIGH): Persistent negative operating cash flow and increasing debtor days could lead to a severe liquidity crunch if order volumes grow.

- Business Model Risk (HIGH): The “jack of all trades, master of none” approach lacks focus and scalability.

- Industry/Competition Risk (HIGH): Intense competition in all segments limits margin expansion.

- Regulatory Risk (MEDIUM): Operations in gems, trading, and infrastructure are subject to various regulatory compliances.

10. Investment Thesis

Bull Case (Why It Can Outperform): If Yaan successfully executes its agri-orders, demonstrates improved cash conversion, and secures a steady pipeline of similar contracts, it could signal a successful pivot. This could lead to a re-rating as a niche agri-logistics player, driving stock price higher. A broader 2026 small-cap rally, as some forecasts suggest, could provide a rising tide.

Bear Case (What Can Go Wrong): The company fails to convert orders into cash profits, margin contraction continues, and the working capital cycle breaks under pressure. The stock, trading at high multiples without fundamental support, could see a sharp correction as news-led excitement fades. Its illiquid nature can amplify the downside.

Key Monitorables for Investors:

- Quarterly Cash Flow from Operations: Turn to positive and sustain.

- Debtor Days: Reduction towards 60 days or below.

- Segment-Wise Disclosure: Clarity on which business is driving profits.

- Order Book Announcements: Sustainability and scale of new orders post the current pipeline.

Clear Conclusion: Yaan Enterprises is a high-risk, event-driven story stock. The recent order wins provide a catalyst, but the underlying financial and business model weaknesses are profound. An investment here is a bet on management’s ability to defy its historical track record and execute a flawless transformation. For most serious investors, the risk-reward balance is unattractive at current valuations. The prudent action would be to wait for concrete evidence of sustained cash flow generation and margin stability before considering an investment from a long-term perspective.

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Our research is conducted solely for educational purposes, so please utilise our knowledge to inform your investment strategy.