MCX Delivers Blowout Q3: 151% Profit Surge Signals Unstoppable Momentum. Is This India’s Most Underrated Growth Stock?

The Multi Commodity Exchange of India Ltd. (MCX) has detonated a financial blockbuster. The Q3 FY26 results, showcasing a 151% year-on-year surge in net profit to ₹401 crore, have sent shockwaves through the market, validating its monopoly and igniting a fierce debate: Is this the start of a BSE-like multi-year rerating, or is the stock, trading at stratospheric valuations, primed for a correction?

This analysis dissects the explosive growth engines, scrutinizes the undeniable premium valuation, and provides a clear-eyed verdict for investors.

The Financial Blowout: Decoding Q3 FY26

The numbers are not just strong; they are record-shattering, painting a picture of a business hitting its operational zenith.

This performance is no accident. It is the result of a strategic trifecta: a near-total monopoly (over 95% market share), a successful push into high-margin options trading, and the launch of innovative products like the MCX BULLDEX index options.

Future Growth Trajectory: Can the Momentum Sustain?

While Q3 is historic, the investment case hinges on the future. Analyst forecasts, though bullish, suggest a moderation from these peak growth rates to a sustained, high-growth trajectory.

The growth levers are visible:

- Market Penetration: Low derivatives penetration in commodities versus equities provides a long runway.

- Product Innovation: Regular launches (indices, minis, sectoral contracts) keep attracting new participants.

- Commodity Super-Cycle: Elevated volatility and prices in bullion and energy boost hedging and trading volumes.

The Billion-Dollar Question: Valuation Versus Quality

Here lies the core of the investment dilemma. MCX’s stellar quality demands a premium, but the current price may have run ahead of even optimistic scenarios.

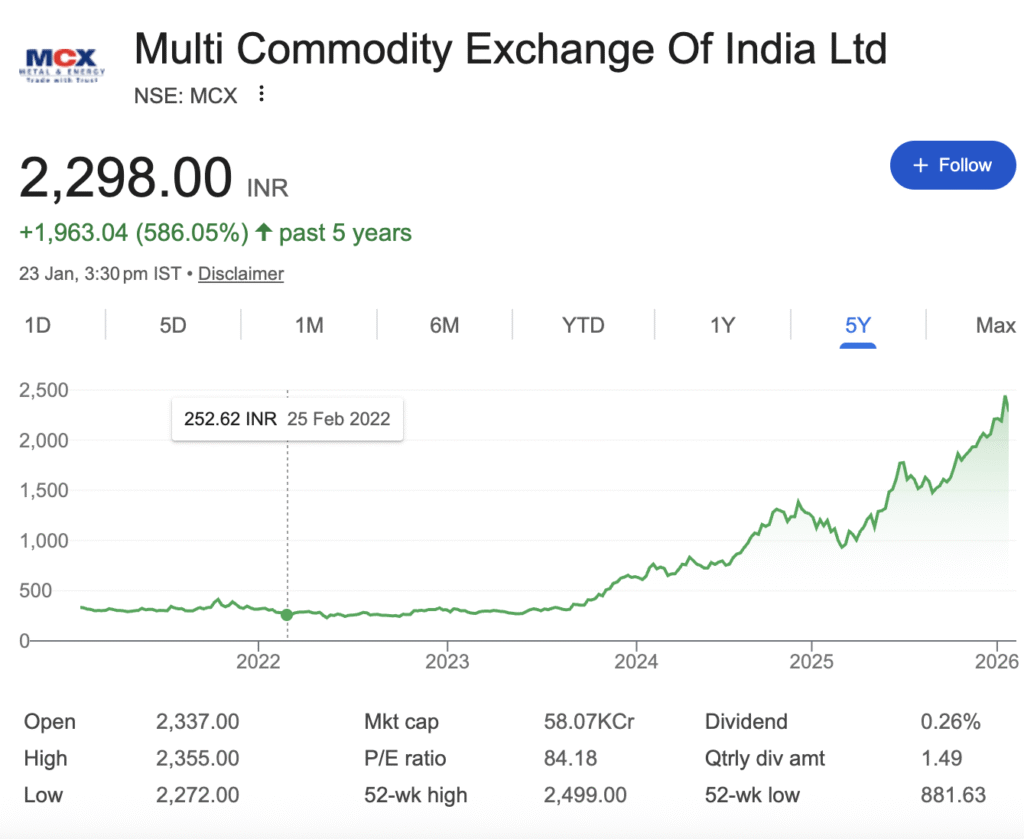

Analyst sentiment reflects this tension. While the long-term story is celebrated, the average 12-month price target of ~₹1,944 – ₹2,256 suggests limited immediate upside from current levels (~₹2,279), with forecasts ranging widely from ₹1,252 to ₹2,625. Notably, recent trading shows a surge in derivatives open interest (+15.88%) coupled with a drop in delivery volume, indicating possible speculative positioning or hedging rather than strong long-term buying conviction.

Investment Verdict: A Strategic Hold, Not a Tactical Buy

For Existing Investors (HOLD): MCX is a crown jewel asset—a profitable, debt-free monopoly in a growing market. The structural story is intact. Volatility is inevitable, but the long-term trajectory favors staying invested. Use any significant market-led corrections to add to holdings.

For New Investors (WAIT for a Better Entry / ACCUMULATE on Dips):

The risk-reward ratio at this all-time high valuation is unfavourable. The business is exceptional, but the margin of safety is thin. Any minor operational hiccup or sectoral rotation could lead to a sharp re-rating.

- Action: Adopt a staggered investment approach. Look for entry points closer to significant technical support levels near ₹2,073 – ₹2,259 or during broader market corrections.

- Watch: Monitor quarterly Average Daily Turnover (ADT) for sustainability, successful new product uptake, and any changes in the competitive or regulatory landscape.

Final Word: MCX has transformed from a simple commodity exchange into a high-tech financial infrastructure platform riding India’s financialization wave. It is the definitive play on the formalization of the commodity markets. However, in the stock market, the price you pay determines your return. At this juncture, patience will likely be rewarded with a more attractive entry point into this outstanding business.

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Our research is conducted solely for educational purposes, so please utilise our knowledge to inform your investment strategy.