Infinity Infoway: 685% Profit Shock & ₹11Cr Govt Jackpot — Is This Nano-Cap SaaS Star a Hidden Gem or a Trap?

The Lead: A Triple-Digit Blowout

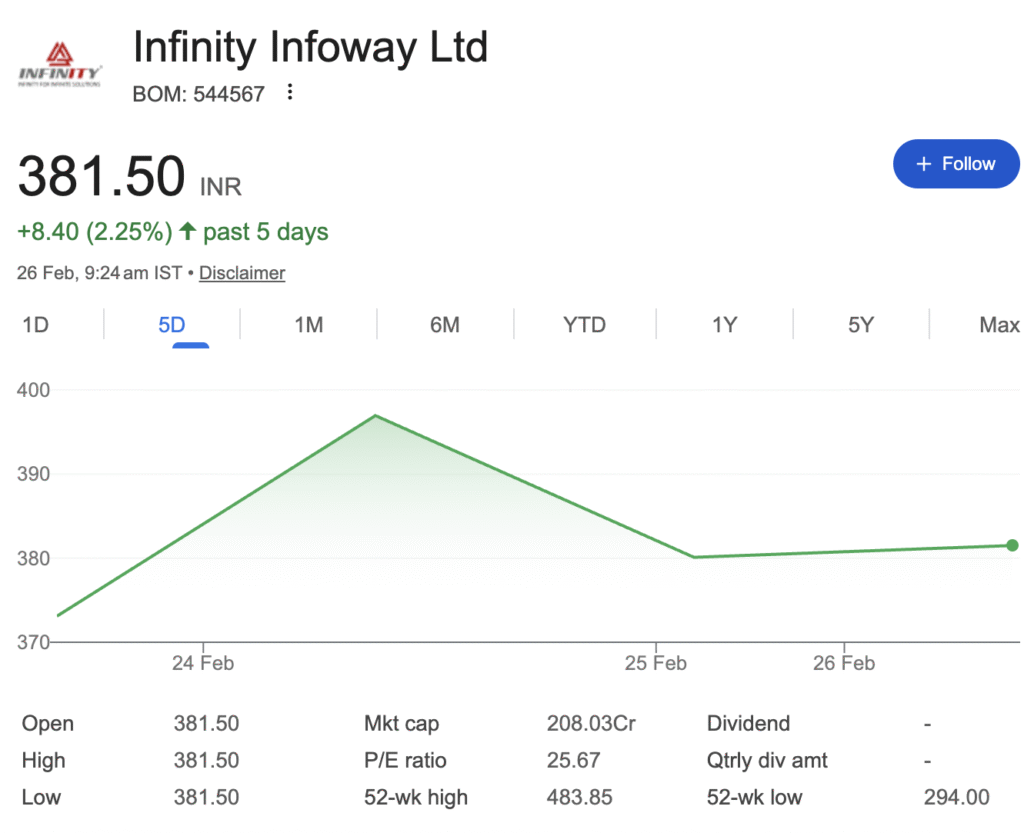

In a quarter where most IT stocks are struggling with margin pressures, Rajkot-based SaaS player Infinity Infoway Ltd (BSE: 544567) has dropped a bomb—and it’s positive. Hot on the heels of winning a ₹10.97 Crore government contract for AI-driven analytics, the company’s quarterly numbers reveal a staggering 685% surge in net profit, leaving Dalal Street analysts scrambling to update their models. But beneath the surface of this 2.25% circuit-hitting stock lies a complex tapestry of explosive growth, premium valuations, and stealthy institutional selling. Is this the next multi-bagger or a classic value trap?

The Catalyst: The Gujarat Government Connection

The immediate trigger for the recent price action is the five-year contract from the Knowledge Consortium of Gujarat. Valued at approximately ₹11 Crore, this project involves setting up a high-end Big Data Analytics platform, complete with AI, Business Intelligence dashboards, and API integrations [citation:user]. Given that the company reported a turnover of just over ₹13 Crore in FY25, this single order represents nearly a full year’s revenue, underscoring its massive materiality

Financial Deep Dive: The 685% Spike Dissected

While the headline news is the contract, the real story is in the quarterly performance reported for December 2025 (Q3 FY26). According to stock analysis data, the company posted a net profit of ₹1.57 Crore for the quarter, a jaw-dropping increase from the mere ₹0.20 Crore reported in the same quarter last year .

To put this in perspective, here is the trajectory of the company’s stellar financial health:

Quarterly Performance Snapshot (in ₹ Crores)

| Particulars | Q3 FY26 (Dec 2025) | Q3 FY25 (Dec 2024) | YoY Change |

|---|---|---|---|

| Sales | ₹6.02 | ₹2.00 | +201% |

| Operating Profit | ₹2.10 | ₹0.35 | +500% |

| Profit After Tax | ₹1.57 | ₹0.20 | +685% |

This isn’t just a one-off beat. The company has shown consistent scaling, with annual revenue growing from ₹5.17 Crore in FY23 to ₹13.19 Crore in FY25—a 155% growth in just two years.

Valuation Matrix: Premium Pricing or Fair Value?

Here is where the debate on Dalal Street heats up. Infinity Infoway is trading at a valuation that commands respect—and scrutiny.

Why the premium P/E? The market is pricing in the high growth trajectory. A P/E of 35x looks steep against the industry, but when juxtaposed with a 685% earnings growth, the PEG (Price/Earnings-to-Growth) ratio actually suggests the stock might still be finding its feet.

The Bear Case & Red Flags

A research analyst’s job is to look beyond the glitter. While the fundamentals are robust, the shareholding pattern reveals a worrying trend.

- Smart Money Exit: Data from the December 2025 quarter indicates that Foreign Institutional Investors (FIIs) have slashed their holdings from 2.60% to just 0.63%. Retail investors also trimmed their positions, dropping from 18.82% to 15.73%.

- Volatility Spike: The stock has an average weekly movement of 8.5% to 9.2%, significantly higher than the Indian Software industry average of 6.6%. For risk-averse investors, this roller-coaster could be unsettling.

- No Dividend, No Coverage: The company pays zero dividends, appealing only to pure growth investors. Furthermore, the stock is covered by zero analysts, meaning there is a lack of institutional consensus or price targets to guide investors.

The Technical Picture

Technically, the stock has returned 30.98% over the past year and an impressive 22.69% over the last three months. However, it remains 27.41% below its 52-week high of ₹483.85, suggesting there is significant overhead resistance. The upper circuit is currently fixed at ₹440, implying a potential 9.5% upside from current levels in the near term.

Peer Comparison: How Does It Stack Up?

To understand if Infinity Infoway is a good investment, we must stack it against its competition in the SME IT space.

| Company | Market Cap (₹ Cr) | Net Profit (₹ Cr) | P/E | ROE (%) |

|---|---|---|---|---|

| Infinity Infoway | 220.85 | 4.0 (TTM) | 34.59 | 47.97 |

| Canarys Automations | 1,137.97 | 17 | ~20 | Moderate |

| Affordable Robotic | 321.77 | 11 | High | Moderate |

| Industry Median | – | – | 27.51 | – |

Analysis: Infinity Infoway is significantly smaller than Canarys but commands a higher ROE, indicating superior profitability on its equity base.

The Verdict:

We look for three things: Growth, Governance, and moat.

- Growth: The 685% profit growth and the ₹11 Crore government contract prove the business model is scalable and trusted by state governments.

- Governance: The management voluntarily disclosed the government contract under Regulation 30 as a measure of “good corporate governance,” which is a positive signal [citation:user].

- Moat: Their specialization in Education ERP and now AI analytics for the public sector creates a niche entry barrier.

The Bottom Line

Infinity Infoway presents a classic high-conviction, high-risk scenario. The bull case rests on explosive earnings growth, a game-changing government contract, and pristine profitability. The bear case hinges on smart money exiting, premium valuations, and the inherent volatility of the nano-cap space.

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Investors are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.