D.P. Abhushan Q3 PAT Soars 96%: Can This Jewellery Stock Shine Brighter in Tier 2 & 3 India?

D.P. Abhushan Ltd (NSE: DPABHUSHAN), an 86-year-old jewellery retailer from Ratlam, has delivered a quarterly performance that is turning heads on Dalal Street. In an environment where elevated gold prices have suppressed industry volumes, the company has reported a staggering 96% year-on-year jump in net profit for Q3 FY26. This explosive growth is not just a flash in the pan but a result of a disciplined strategy focused on Tier 2 & 3 cities, operational efficiency, and a sharp diversification into silver and diamonds. As the stock experiences significant volatility, trading ~28% below its 52-week high, investors are keenly assessing whether this regional champion is a golden opportunity or a value trap

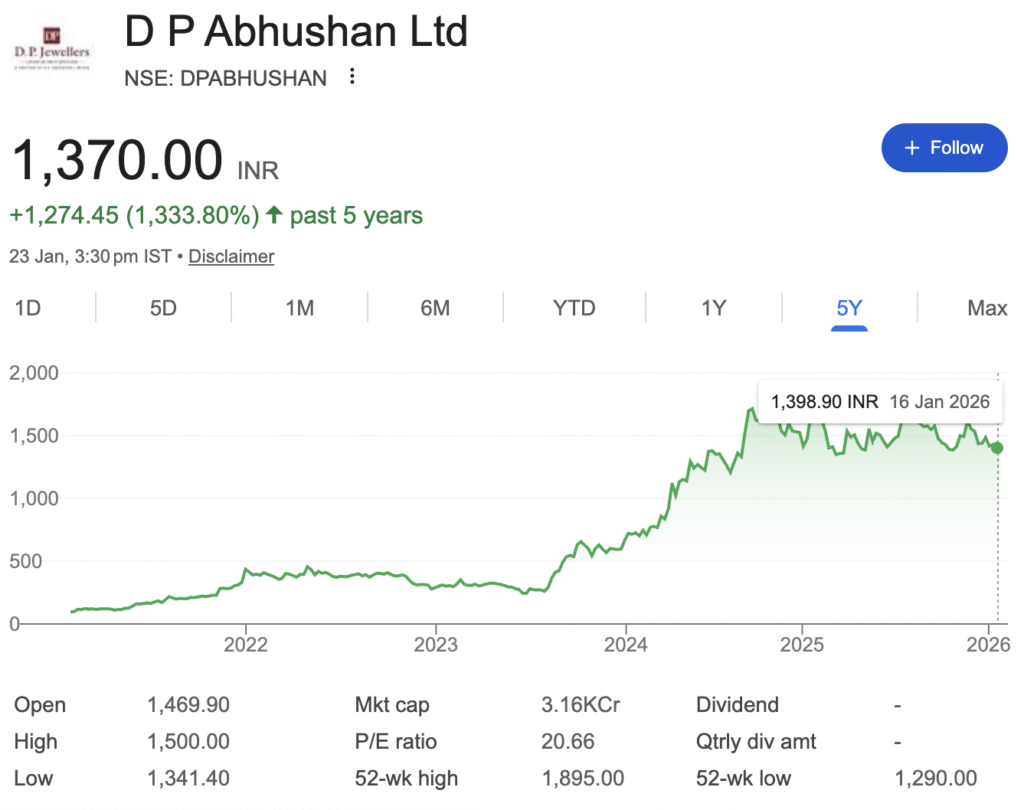

The stock, already a multibagger with a 333.8% return over the past five years, continues to draw investor attention. But with gold prices at elevated levels and consumer demand turning selective, the critical question is: does DP Abhushan have the financial stamina and strategic clarity to sustain this momentum?

The Financial Firepower: A Deep Dive into the Numbers

The Q3 and Nine-Month (9M) FY26 results reveal a company not just growing, but transforming its profitability profile.

Table 1: Consolidated Financial Snapshot (₹ Crores)

| Metric | Q3 FY26 | Q3 FY25 | YoY Change | 9M FY26 | 9M FY25 | YoY Change |

|---|---|---|---|---|---|---|

| Total Revenue | 1,222.37 | 1,085.17 | +13% | 2,731.44 | 2,594.70 | +5.3% |

| Gross Profit | 136.99 | 84.96 | +61.2% | 320.54 | 200.14 | +60.2% |

| Gross Margin (%) | 11.21% | 7.83% | +338 bps | 11.74% | 7.71% | +403 bps |

| EBITDA | 105.63 | 55.80 | +89.3% | 236.68 | 132.14 | +79.1% |

| EBITDA Margin (%) | 8.64% | 5.14% | +350 bps | 8.67% | 5.09% | +358 bps |

| Profit After Tax (PAT) | 73.35 | 37.34 | +96.4% | 161.24 | 87.54 | +84.2% |

| PAT Margin (%) | 6.00% | 3.44% | +256 bps | 5.90% | 3.37% | +253 bps |

Source: Company Investor Presentation

What the numbers tell us:

The standout story is margins. Revenue growth is healthy, but the explosive profit growth is driven by a significant expansion in profitability at every level—gross, EBITDA, and PAT. This suggests superior inventory management, product mix enhancement (more diamonds and silver), and operating leverage kicking in as the store network matures.

Operational Excellence: The Engine Behind the Growth

- High-Throughput Stores: The company boasts an impressive Average Revenue per Sq.Ft of ~₹5.39 Lakhs (9MFY26) and a high Inventory Turnover Ratio of 4.5x (Annualised), indicating efficient space utilization and faster stock movement.

- Wedding & Trust Anchor: Despite high gold prices, demand from wedding buyers remained resilient. The company’s deep regional trust, built over generations, allows it to command loyalty.

- Silver & Diamonds – New Growth Avenues: Management highlighted silver as a key driver, catering to festive gifting and affordability. Their strategic “World of Diamonds” exhibitions aim to increase the share of high-margin diamond jewellery from 6% to 15% of revenue.

- Strategic Expansion: Following the recent opening of stores in Ajmer, Neemuch, and a second showroom in Ratlam, the roadmap is clear—aggressive COCO (Company Owned Company Operated) expansion in Madhya Pradesh, Rajasthan, Gujarat, and Chhattisgarh over the next five years.

📈 Recent Stock Moves & Valuation Context

The stock has been on a rollercoaster. After touching a 52-week high of ₹1,895 in November 2025, it has corrected sharply and is currently trading around ₹1,372. This represents a decline of approximately 19% over the past year, underperforming the broader small-cap indices during this period.

Table 2: Peer Valuation & Financial Comparison

Valuation Insights:

- D.P. Abhushan trades at a significant discount to large organized players like Titan on a P/E basis, but at a premium to some regional peers when considering its superior Return on Equity (ROE).

- Its ROE of over 35% is the highest among the peer set shown, indicating exceptional efficiency in generating profits from shareholder capital.

- Some fundamental analysis sites flag the stock as potentially “overvalued” based on intrinsic value models, suggesting the recent price correction may be a market reassessment of its growth premium.

🚀 Growth Prospects & Strategic Roadmap

Management has laid out an ambitious yet calibrated expansion plan:

- Geographic Expansion: The company, currently present in 11 stores across MP and Rajasthan, plans to enter Gujarat, Chhattisgarh, and Maharashtra, adding 3-5 stores annually. The focus remains on high-potential Tier 2 & 3 cities.

- Revenue Ambition: For FY26, the company is targeting a revenue of ₹3,900-4,000 crore, up from ₹3,300 crore in FY25, representing growth of 18-21%.

- Product Mix Enhancement: A strategic initiative aims to increase the share of high-margin diamond-studded jewellery from about 6% to 15% of revenue, leveraging exhibitions and new collections.

- Funding Growth: Expansion will be funded through internal accruals and a planned QIP (Qualified Institutional Placement) of ~₹600 crore, aiming to keep debt (currently ₹170-180 crore) in check.

⚖️ Should You Invest? The Bull vs. Bear Debate

The Bull Case:

- Superior Financials: Exceptional profit growth, industry-leading margins and ROE, and strong cash generation from operations.

- Right Market Focus: Dominant positioning in the high-growth, less penetrated Tier 2/3 markets of Central India.

- Scalable Model: Proven company-owned, company-operated (COCO) model with efficient centralized procurement, ready for replication in new regions.

- Favourable Industry Tailwinds: The organized jewellery retail segment is projected to grow significantly, and India’s overall jewellery market is expected to reach ~$154 billion by 2033.

The Bear Case & Key Risks:

- Commodity Price Risk: Earnings remain vulnerable to sharp fluctuations in gold and diamond prices, which can impact consumer demand and inventory values.

- Execution Risk: Successful integration and profitability of new stores in unfamiliar territories is not guaranteed and could strain management resources.

- Valuation Concerns: Despite the correction, some analysts consider the stock expensive based on intrinsic value estimates, and its premium to book value (P/B of ~7.9) is high.

- High Promoter Ownership & Liquidity: The stock may exhibit higher volatility due to relatively lower public float.

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Our research is conducted solely for educational purposes, so please utilise our knowledge to inform your investment strategy.