BCC Fuba India’s Micro-Cap Gambit: A ₹5.1 Lakh Bet to Dominate the Electronics Manufacturing Wave – Smart Strategy or Penny Stock Play?

In a strategic move that underscores the fierce competition in India’s electronics manufacturing landscape, BCC Fuba India Limited (BSE: 517246) has formally announced the acquisition of a 51% controlling stake in Iogems Technologies Private Limited (ITPL). Priced at a seemingly nominal ₹5.1 lakh, this acquisition is a deliberate play for forward integration. But does this micro-cap transaction signal macro-cap ambition for BCC Fuba’s investors? We conduct a bottom-to-top analysis, peeling back the layers of this PCB manufacturer’s finances and future.

The Acquisition Decoded: More Than Meets the Eye

On January 23, 2026, BCC Fuba crossed a strategic threshold. ITPL, incorporated barely three months prior in October 2025, is a clean slate—no turnover, no historical baggage. This isn’t a turnaround story; it’s a greenfield venture in disguise. By purchasing 51,000 shares at par value (₹10 each), BCC Fuba isn’t just buying a company; it’s purchasing a vehicle to enter the high-growth Electronic Manufacturing Services (EMS) segment.

The logic is clear: leverage their core competency in Printed Circuit Board (PCB) manufacturing to move up the value chain. Instead of just supplying components, they now aim to assemble finished electronic products. In an era of PLI schemes and ‘Make in India’, this vertical integration could be a masterstroke, potentially capturing more margin per unit and reducing dependency on downstream players.

This strategic pivot aligns perfectly with a once-in-a-generation megatrend. India’s EMS sector is projected to explode from $33 billion in 2024 to a staggering $155 billion by 2030, a compound annual growth rate (CAGR) of 30%. Concurrently, the domestic PCB market is forecast to grow from $3.5 billion to $8.2 billion by 2030. By positioning itself in the middle of this value chain, BCC Fuba seeks to leverage its PCB expertise to secure a larger slice of the electronics manufacturing pie, driven by government Production Linked Incentive (PLI) schemes and rising domestic demand.

Financial Health Check: Stability Meets Growth

A deep dive into BCC Fuba’s financials reveals a company in a turnaround phase, transitioning from past struggles to recent profitability.

The most compelling narrative in the financials is the remarkable margin expansion. From operating at a loss a decade ago, the company has steadily improved its operational efficiency, now boasting a robust OPM of over 15%. This is supported by a consistent rise in reserves and surplus on the balance sheet, from ₹0.37 crores in Mar’23 to ₹7.85 crores in Mar’25. However, this positive trend is juxtaposed against a sky-high P/E ratio, suggesting the market has already priced in a perfect growth trajectory.

The Valuation Conundrum and Sector Context

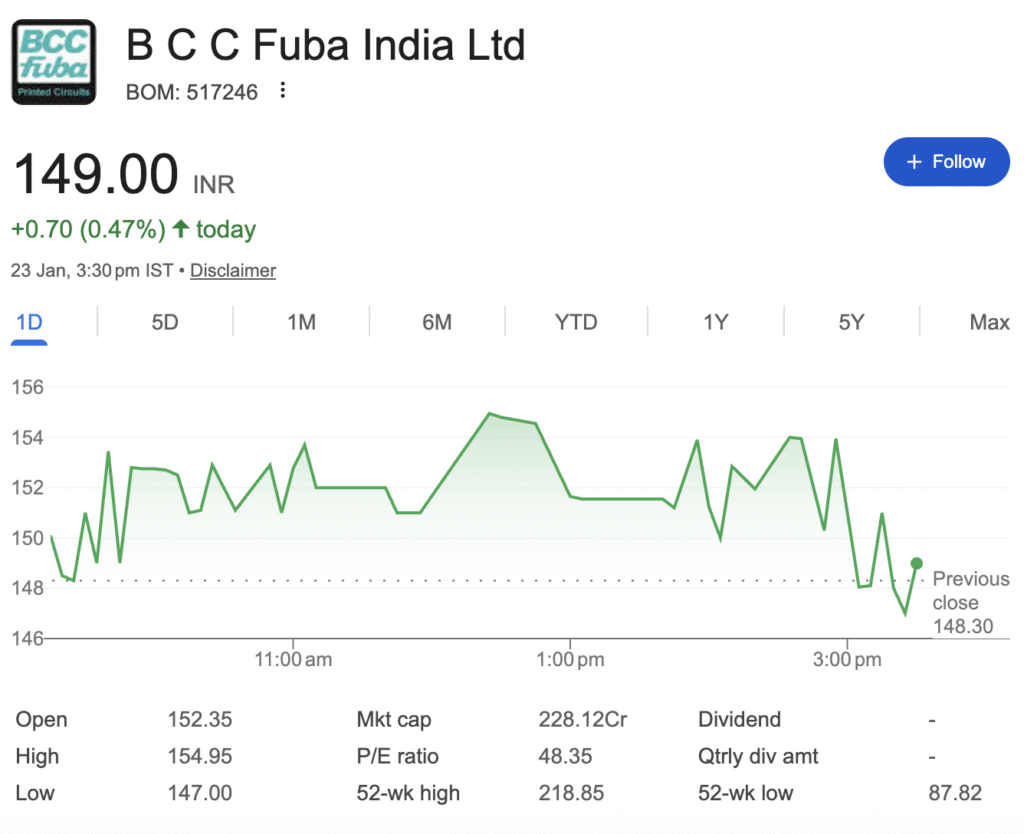

With a P/E of 48, BCC Fuba appears expensive. However, context is crucial. The entire Indian EMS sector has commanded premium valuations due to its hyper-growth prospects. For instance, leaders like Kaynes Technologies have traded at an EV/EBITDA of 58.4x.

Yet, recent months have seen a sector-wide de-rating. Companies like Dixon Technologies and PG Electroplast have faced stock price corrections due to high-base effects, temporary demand softness, and valuation fatigue. This macro backdrop means BCC Fuba is expanding into a sector where investor expectations are being recalibrated, and execution is now scrutinized more than ever.

BCC Fuba’s primary challenge is scale. Its annual revenue (TTM ₹586.32M) is a fraction of its listed peers. The Iogems acquisition, while strategically sound, is financially immaterial. The real test will be the company’s ability to scale this EMS venture rapidly, which may require significant capital expenditure. The formation of a Fund-Raising Committee in December 2025 indicates the management is preparing for this next phase.

Investment Verdict: High-Risk, High-Potential Satellite Holding

For Aggressive, Risk-Tolerant Investors: SPECULATIVE BUY.

BCC Fuba presents a high-risk, high-reward proposition. You are investing in a micro-cap turnaround story with improving fundamentals, making a timely strategic move into a secular growth megatrend. If the company successfully executes its EMS foray and leverages the sector tailwinds, the upside potential from its small base could be substantial. It should be treated strictly as a satellite holding within a diversified portfolio.

For Conservative, Income-Seeking Investors: AVOID.

This is not a stable, dividend-paying blue chip. The high valuation, micro-cap liquidity risks, low promoter holding, and the sheer execution risk of building a new business segment make it unsuitable for conservative portfolios. The sector’s recent de-rating also adds near-term headwinds.

The Bottom Line

BCC Fuba India is attempting a savvy pivot at the right macroeconomic moment. Its improving financial health provides a stable base, and the EMS strategy is directionally correct. However, the stock’s premium valuation leaves little room for error. Investors should closely monitor subsequent quarterly statements for evidence of EMS revenue traction, margin performance, and details on the fund-raising committee’s actions. In the high-stakes race of Indian electronics manufacturing, BCC Fuba has signalled its intent; the market now awaits proof of execution.

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Our research is conducted solely for educational purposes, so please utilise our knowledge to inform your investment strategy.