Aurobindo Pharma’s Philippines Foray: A Strategic Expansion or Just Another Subsidiary? We Dive Deep Into the Financials & Future Outlook

In a regulatory filing to the stock exchanges on Thursday, pharmaceutical major Aurobindo Pharma Ltd. announced that its Netherlands-based wholly-owned subsidiary, Helix Healthcare B.V., has incorporated a new fully-owned arm in the Philippines—Aurobindo Pharma Philippines Inc. The move, involving an initial capital subscription of approximately $2 million, marks another step in the company’s ongoing strategy to deepen its presence in key global growth markets. But beneath this corporate development lies a critical question for investors: does Aurobindo’s current financial health and growth trajectory justify investment, especially after a period of stock price consolidation?

The Strategic Move: More Than Just Paperwork

The incorporation, effective January 23, 2026, is a classic Aurobindo tactic—using a step-down subsidiary structure for market entry. The stated object is to expand the pharmaceutical products business in the Philippines, a growing ASEAN market with increasing healthcare expenditure. With no governmental approvals required, the company can move swiftly. This aligns with Aurobindo’s established playbook of building a sprawling global network for generics and active pharmaceutical ingredients (APIs).

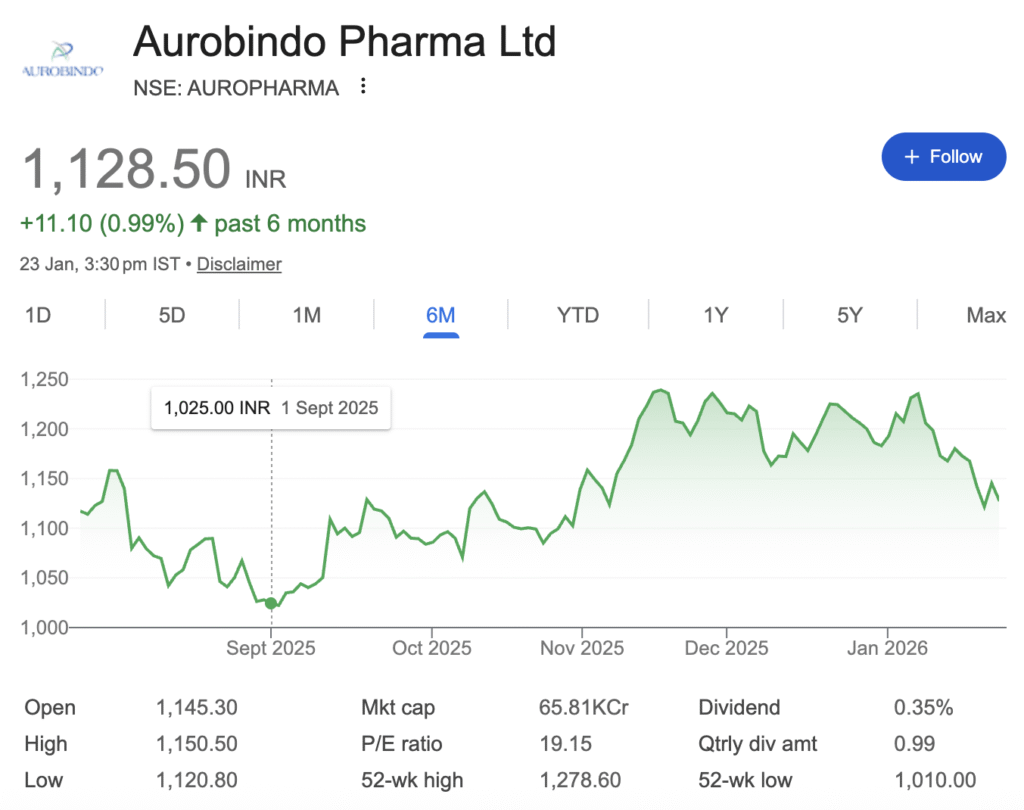

📊 Valuation Snapshot: The Market’s Current Verdict

The table below breaks down the key financial metrics painting the picture of Aurobindo Pharma’s current market standing.

🚀 Growth Engines and Strategic Plays

The bearish price action contrasts sharply with several positive fundamental developments and future growth levers.

- Strong Financial Forecasts: Analysts project earnings to grow at 15.8% per annum over the coming years, with EPS growth at 15.4%. Revenue is forecast to reach nearly ₹400,232 crore by March 2028.

- Recent Operational Beat: The company’s Q1 FY25 earnings were a standout, with revenue up 10% YoY and net profit surging 61% YoY to ₹919 crore. Management has confidently reaffirmed its FY25 EBITDA margin guidance of 21-22%.

- Strategic Expansion: January 2026 has been a month of active growth strategy. Following the recent acquisition of Khandelwal Laboratories’ branded business for ₹325 crore to bolster its domestic footprint, the company has now formed Aurobindo Pharma Philippines Inc., a wholly-owned step-down subsidiary, to tap into the ASEAN market.

⚠️ Navigating the Risk Landscape

Investors’ caution is not unfounded, as the company navigates a sector fraught with regulatory scrutiny.

- Ongoing USFDA Oversight: The company’s subsidiary, APL Healthcare, recently received a Form 483 with five observations from the USFDA for its Andhra Pradesh unit. Another facility in Telangana received three observations earlier in December. While the company has classified these as “procedural” and stated they do not impact current operations or financials, such events introduce an overhang of regulatory risk that often weighs on pharma valuations.

📈 Growth vs. Risk: The Investment Thesis Balance

🧭 Analyst Sentiment and Final Verdict

The analyst community leans decidedly bullish, seeing the current price as a disconnect from fundamentals. A significant 82.14% of analysts rate the stock a ‘BUY’, with an average 12-month target price of ₹1,306.64. Other aggregations suggest an even higher average target of ₹1,353.03.

| Analyst Consensus | Rating | Average Price Target | Implied Upside |

|---|---|---|---|

| Based on 28 Analysts | 82.14% BUY | ₹1,306.64 | +14.09% |

Investment Conclusion: A Cautious for the Patient Investor

Aurobindo Pharma presents a compelling case of “value with growth” currently masked by regulatory noise and short-term market pessimism. The stock is not without risk—any escalation in USFDA issues could further pressure the share price.

However, for investors with a medium- to long-term horizon who can tolerate regulatory volatility, the current levels offer an attractive entry point. The combination of a discounted valuation, strong forecasted earnings growth, and proactive strategic expansion creates a favourable risk-reward asymmetry.

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Our research is conducted solely for educational purposes, so please utilise our knowledge to inform your investment strategy.