Meta Infotech: Just Secured 3 Separate Order Today, 55% Revenue CAGR, But Why Is This Cybersecurity Stock Down 77%?

On the last day of the fiscal year, Meta Infotech Ltd. (BSE: 544441) did something unusual. It dropped three separate order confirmation announcements totalling ₹5.87 crore into the stock exchange. Email security. Cloud data protection. Annual subscriptions. All from domestic financial services players and a large conglomerate.

On any other day, this would be a straightforward positive. But for Meta Infotech, the story isn’t that simple.

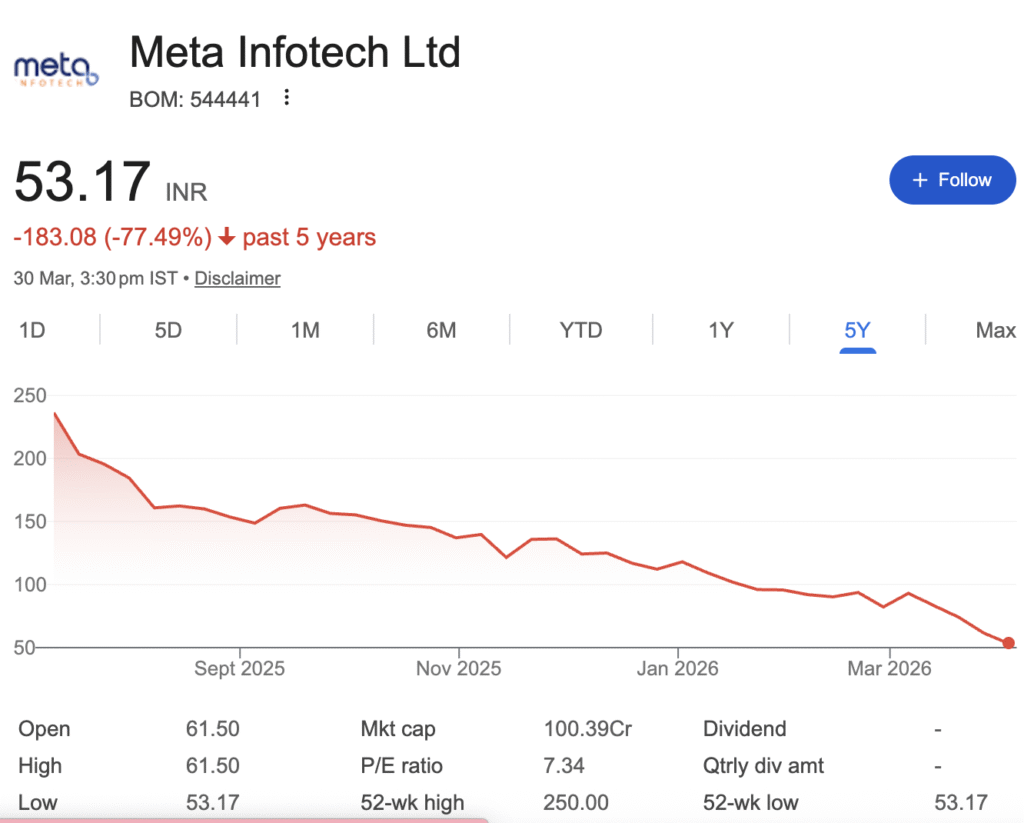

The company currently holds an outstanding order book of ₹573 crore—a staggering 2.62 times its FY25 revenue. Yet, the stock has plummeted 77% from its 52-week high of ₹250, currently trading at ₹53.

What’s going on? Is this a classic case of market overreaction creating a buying opportunity? Or are there deeper issues that warrant caution?

Let’s dig into the numbers.

The Financial Picture: Growth With a Catch

Meta Infotech’s financial trajectory tells a story of remarkable expansion—but the latest chapters reveal emerging cracks.

📊 5-Year Financial Performance At a Glance

| Particulars | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Revenue (₹ Cr) | 42 | 77 | 110 | 152 | 218 |

| Revenue Growth (%) | — | 83% | 43% | 38% | 43% |

| Operating Profit (₹ Cr) | 3 | 6 | 11 | 17 | 24 |

| Net Profit (₹ Cr) | 1 | 3 | 7 | 11 | 16 |

| Net Profit Growth (%) | — | 200% | 133% | 57% | 45% |

| EPS (₹) | 18 | 1.76 | 3.71 | 5.96 | 8.22 |

Key Ratios That Matter

| Metric | FY2024 | FY2025 | Industry Average | Verdict |

|---|---|---|---|---|

| ROE (%) | 42.39% | 38.87% | 15-20% | ✅ Exceptional |

| ROCE (%) | 52.33% | 45.68% | 18-22% | ✅ Outstanding |

| Net Profit Margin (%) | 6.91% | 6.63% | 8-10% | ⚠️ Slightly Below |

| Debt to Equity | 0.17 | 0.24 | 0.5-0.8 | ✅ Low Leverage |

| P/E Ratio | — | 7.8-13.5x | 26.7x (Industry) | ✅ Deep Discount |

The Growth Story: What the Numbers Tell Us

The Good:

- 55% Revenue CAGR over five years—from ₹41 crore in FY2021 to ₹218 crore in FY2025

- 64% Profit CAGR during the same period, indicating operating leverage kicking in

- ROE of 38.87% —for context, anything above 20% is considered excellent in the IT services space

- Order book of ₹573 crore providing revenue visibility for the next 2-3 years

The Concerning:

- Operating cash flow turned negative at -₹12.74 crore in FY2025, compared to +₹34.51 crore in FY2023

- Debt has actually increased post-IPO—long-term borrowings rose from ₹3.2 crore to ₹7.9 crore, short-term from ₹14.2 crore to ₹24.2 crore

- Margin compression—EBITDA declined 16% YoY in H1FY26 despite 14% revenue growth

The IPO, launched in July 2025 at a price band of ₹153-161, listed at a 39.8% premium but has since been on a downward spiral. The question is: does the market see something the income statement isn’t revealing?

The ₹573 Crore Order Book: Real Value or Mirage?

This is where the analysis gets interesting—and where the bull case gains serious weight.

Orders vs. Market Cap: A Statistical Anomaly

| Metric | Value |

|---|---|

| Market Cap (as of March 2026) | ₹101 crore |

| Outstanding Order Book | ₹573 crore |

| Order Book / Market Cap | 5.67x |

| Order Book / FY25 Revenue | 2.62x |

For a micro-cap company (market cap under ₹500 crore), an order book that’s more than double its current valuation is exceptionally rare. In the cybersecurity services space, this typically signals one of three things:

- Undervaluation — the market hasn’t priced in future revenue

- Execution risk — doubts about the company’s ability to deliver

- Margin concerns — fears that these orders won’t translate to proportional profits

Management claims the order book is “largely driven by the banking segment, followed by NBFCs and capital market clients”—a financially strong and sticky customer base.

The H1FY26 Revenue Anomaly

Here’s something that jumps off the page:

| Period | Revenue (₹ Cr) |

|---|---|

| FY2025 (Full Year) | 218 |

| H1FY26 (Six Months) | 210 |

Meta Infotech earned nearly as much in the first half of FY2026 as it did in all of FY2025. The company’s revenue run rate has effectively doubled.

If this trajectory sustains, FY2026 revenue could cross ₹400 crore—a near-doubling from FY2025 levels. At that scale, with even a 6% net margin, net profit would exceed ₹24 crore.

The Red Flags: Why the Market Is Skeptical

No analysis is complete without addressing the concerns that have driven the stock down 77% from its peak.

🚩 Cash Flow Deterioration

| Year | Operating Cash Flow (₹ Cr) |

|---|---|

| FY2023 | +34.51 |

| FY2024 | -3.77 |

| FY2025 | -12.74 |

A company can report accounting profits while burning cash—and that’s exactly what’s happening here. Negative operating cash flow for two consecutive years raises legitimate questions about working capital management and collection efficiency.

🚩 The Debt Paradox

The company’s IPO prospectus stated that ₹15.35 crore of IPO proceeds were earmarked for debt repayment. Yet:

- Short-term borrowings: ₹14.2 crore (FY2024) → ₹24.2 crore (Sept 2025)

- Long-term borrowings: ₹3.2 crore (FY2024) → ₹7.9 crore (Sept 2025)

Management’s explanation? “Higher bill discounting at attractive rates to manage a temporary delay in payments from a key customer”.

This explanation has two interpretations:

- Bullish view: Prudent use of short-term financing to bridge a one-time timing gap

- Bearish view: IPO proceeds didn’t solve the underlying cash conversion cycle problem

🚩 Margin Pressure

| Metric | H1FY25 | H1FY26 | Change |

|---|---|---|---|

| EBITDA (₹ Cr) | 19 | 16 | -16% |

| Net Profit (₹ Cr) | 11 | 10 | -9% |

Despite 14% revenue growth, both EBITDA and net profit contracted in H1FY26. Management attributes this to “strategic investments in talent and geographic expansion”.

The Business Model: Why Cybersecurity Is the Right Sector

Meta Infotech isn’t your typical IT services company. It’s a pure-play cybersecurity solutions provider operating in one of the fastest-growing segments in enterprise technology.

Revenue Segmentation (H1FY26)

| Segment | Contribution (₹ Cr) |

|---|---|

| SASE (Secure Access Service Edge) | 159.5 |

| DAM (Database Security) | 26.9 |

| EDR (Endpoint Detection & Response) | 5.2 |

| Sustenance Services | 7.8 |

| Professional Services | 5.9 |

| Managed Security Services | 2.4 |

The diversified revenue mix—70%+ from SASE products, with the remainder from services—provides both scale and margin stability.

Why This Matters

The Indian cybersecurity market is projected to grow at 15-20% annually, driven by:

- RBI mandates for banks and NBFCs on cybersecurity frameworks

- Increasing digitization across sectors

- Rising threat landscape making security non-discretionary

Meta Infotech serves 874 enterprise customers across 15 industries, including banking, capital markets, insurance, and manufacturing. Its customer base is both diversified and financially strong.

The Bull Case

- Staggering order book: ₹573 crore vs. ₹101-235 crore market cap creates asymmetric upside potential

- Revenue acceleration: H1FY26 revenue of ₹210 crore already matches FY2025 full year

- Exceptional profitability metrics: ROE of 38-42% and ROCE of 45-52% are world-class

- Deep valuation discount: P/E of 7-13x vs. industry average of 27x

- Secular tailwinds: Cybersecurity spending is non-discretionary and growing

The Bear Case

- Cash flow deterioration: Two years of negative operating cash flow

- Post-IPO debt increase: Borrowings rose despite IPO proceeds for repayment

- Margin compression: EBITDA and PAT declined in H1FY26 despite revenue growth

- Execution risk: Can the company deliver on the ₹573 crore order book profitably?

- Micro-cap volatility: Low liquidity and high price swings

From a pure fundamental perspective, Meta Infotech presents a classic value trap vs. deep value dilemma:

- If the company can convert its order book into profitable revenue while managing working capital, the current valuation represents a significant buying opportunity.

- If cash flow issues persist and margins continue to compress, the stock could test lower levels.

The company’s July 2025 IPO was a coming-of-age moment, but the post-listing performance suggests the market is in a “show me” mode. Promoter holding remains elevated at 68.90% —a sign of confidence, but also a reminder that this remains a promoter-driven business.

For New Investors

Wait for clarity on three fronts:

- Cash flow turnaround: Look for positive operating cash flow in the next 1-2 quarters

- Debt stabilization: Borrowings should not increase further post-IPO

- Margin bottoming: EBITDA margins need to stabilize or improve

The Bottom Line

Meta Infotech is a business with exceptional growth metrics, a staggering order book, and a deep valuation discount—but also with legitimate cash flow concerns and margin pressures.

At current levels, this isn’t a stock for conservative investors. For those with high risk tolerance and a long-term horizon, it represents a speculative opportunity in one of India’s fastest-growing cybersecurity firms.

Key Catalyst to Watch: Next quarterly results (likely May-June 2026). If cash flow turns positive and margins stabilize, expect a sharp re-rating.

Source: Trade Brains, CNBC TV18, ScanX, BlinkX

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Investors are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.