Talbros Automotive: A Rs 1,000 Crore Order Ignites Rally, But Is The Stock Running Too Hot?

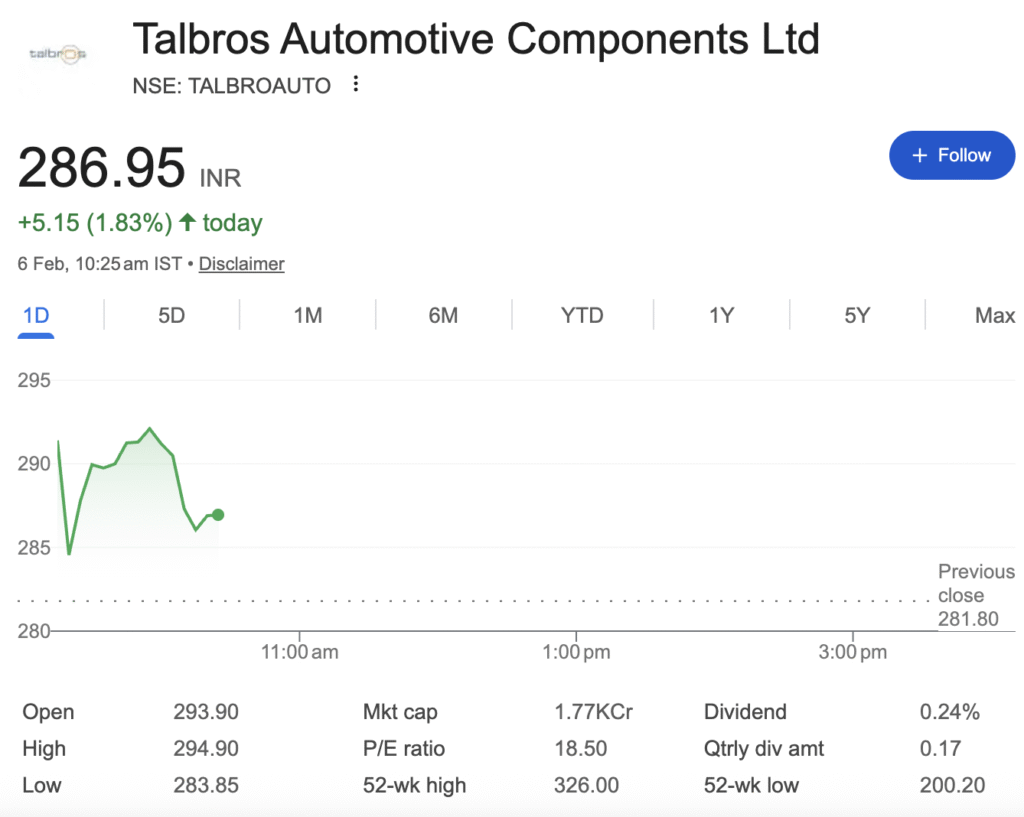

The stock of Talbros Automotive Components Ltd (NSE: TALBROAUTO) surged over 2% in early trade today, significantly outperforming a flat broader market, on the back of a blockbuster business announcement. The auto ancillary player, along with its joint ventures, has secured multi-year orders worth over ₹1,000 crores from leading domestic and international OEMs, promising a substantial boost to its revenue visibility starting FY27

This mega order win, equivalent to approximately 60% of its trailing twelve-month revenue, has rightfully captured investor attention. However, beneath the euphoria lies a more complex financial picture. A bottom-to-top analysis reveals a company at a strategic inflection point: boasting a robust order book and a healthy balance sheet, but also grappling with near-term margin pressures and a valuation that appears stretched against historical benchmarks.

Decoding the Mega Order: A Five-Year Growth Engine

The orders, to be executed over the next five years, provide a clear roadmap for Talbros’ growth and diversification.

- Forging a Global Path: The largest chunk, worth ₹500 crores, comes from the forgings business and is primarily for exports. A key win includes a new major European automotive component supplier, underscoring Talbros’ global competitiveness.

- Riding the EV Wave: In a significant strategic move, the company, through its JV Marelli Talbros Chassis Systems, secured ₹90 crores in orders for Body-in-White (BIW) components destined for luxury electric SUVs.

- Domestic Consolidation: The joint venture Talbros Marugo Rubber secured ₹170 crores in domestic orders for hoses and anti-vibration parts, while the sealing division added another ₹250 crores in orders for gaskets and heat shields.

This diversified order book strengthens Talbros’ position across traditional and new-age automotive segments, with commercialization set to begin from FY27.

Financial Health Check: Resilience Meets Margin Pressure

While the future looks promising, the recent financial performance shows a mixed trend. The company is scheduled to announce its Q3 FY26 results on February 11, which will be a crucial indicator of current operational health.

Recent Financial Performance (Consolidated):

Calculated from the provided EBIDTA and Revenue figures.

On the positive side, Talbros maintains a strong balance sheet with low debt. The consolidated debt-to-equity ratio stood at a comfortable 0.13 as of March 2025, providing financial flexibility to ramp up capacity for new orders. The company also generates positive cash flow from operations, which was ₹80 crore in FY25.

However, management commentary from the Q1 FY26 earnings call highlights challenges. The forging segment saw muted growth due to delayed export orders, and the domestic business faced headwinds from delayed vehicle launches by key customers like Maruti. This has kept near-term revenue growth in low single digits.

Valuation: The Premium Price Tag

This is where the investment debate intensifies. The recent rally has pushed the stock’s valuation to a premium.

- The stock currently trades at a P/E ratio between 17.2x to 22.8x (TTM), which is reasonable compared to the sector P/E of 44.5.

- However, intrinsic value models suggest caution. Independent analysis estimates the stock’s median fair value at around ₹100.88, based on historical EV/EBITDA, EV/Sales, and Price/Sales models, implying the current price of ~₹287 is significantly overvalued.

- Technical analysts note the stock is in a strong momentum phase, trading above all key moving averages after a series of gains, but warn of high intraday volatility (beta of 1.29) and mixed underlying technical indicators.

Growth Prospects & Strategic Positioning

The future growth narrative rests on three pillars:

- Execution of the ₹1,000+ Crore Order Book: Successful commercialization from FY27 will be the single biggest driver, potentially adding an average of ₹200+ crore to annual revenues.

- Export-Led Expansion: Management aims to increase export contribution from 28% (Q1 FY26) to near 35% of revenue, leveraging new relationships in Europe and other regions.

- Electric Vehicle Integration: The orders for EV-specific BIW components position Talbros in the high-growth EV supply chain, a critical long-term diversification.

Investment Verdict: A Calculated Gamit on Future Execution

Should we invest in Talbros Automotive Components?

The answer is not a simple yes or no, but a conditional one based on your investment horizon and risk appetite.

- For Long-Term Investors (Horizon: 3-5 Years): The case is compelling. The massive order book provides unprecedented revenue visibility, the balance sheet is robust, and the foray into the EV segment is strategically sound. This stock could be considered for a small, strategic allocation with a strict focus on the long term. The key monitorable will be the sequential improvement in margins and the timely execution of the announced orders starting FY27.

- For Short-Term Traders & Risk-Averse Investors: Exercise extreme caution. The stock appears overvalued based on several intrinsic value estimates and is reacting to news that will materialize in future years. Near-term headwinds in certain business divisions and rich valuations leave little margin for error. The high beta also means the stock is likely to be more volatile than the market.

The Bottom Line: Talbros Automotive has successfully scripted a promising future chapter with its landmark order win. However, the present chapter shows a company navigating cyclical pressures. The market is clearly paying today for the growth it expects tomorrow. Investors betting on this story must have the patience to see it through the next few quarters of potentially uneven performance and the conviction that management will deliver on its sizable promises.

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Our research is conducted solely for educational purposes, so please utilise our knowledge to inform your investment strategy. Investors are advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.