From Humble Seeds to Market Beast: A Deep Dive into Narmada Agrobase’s Meteoric Rise

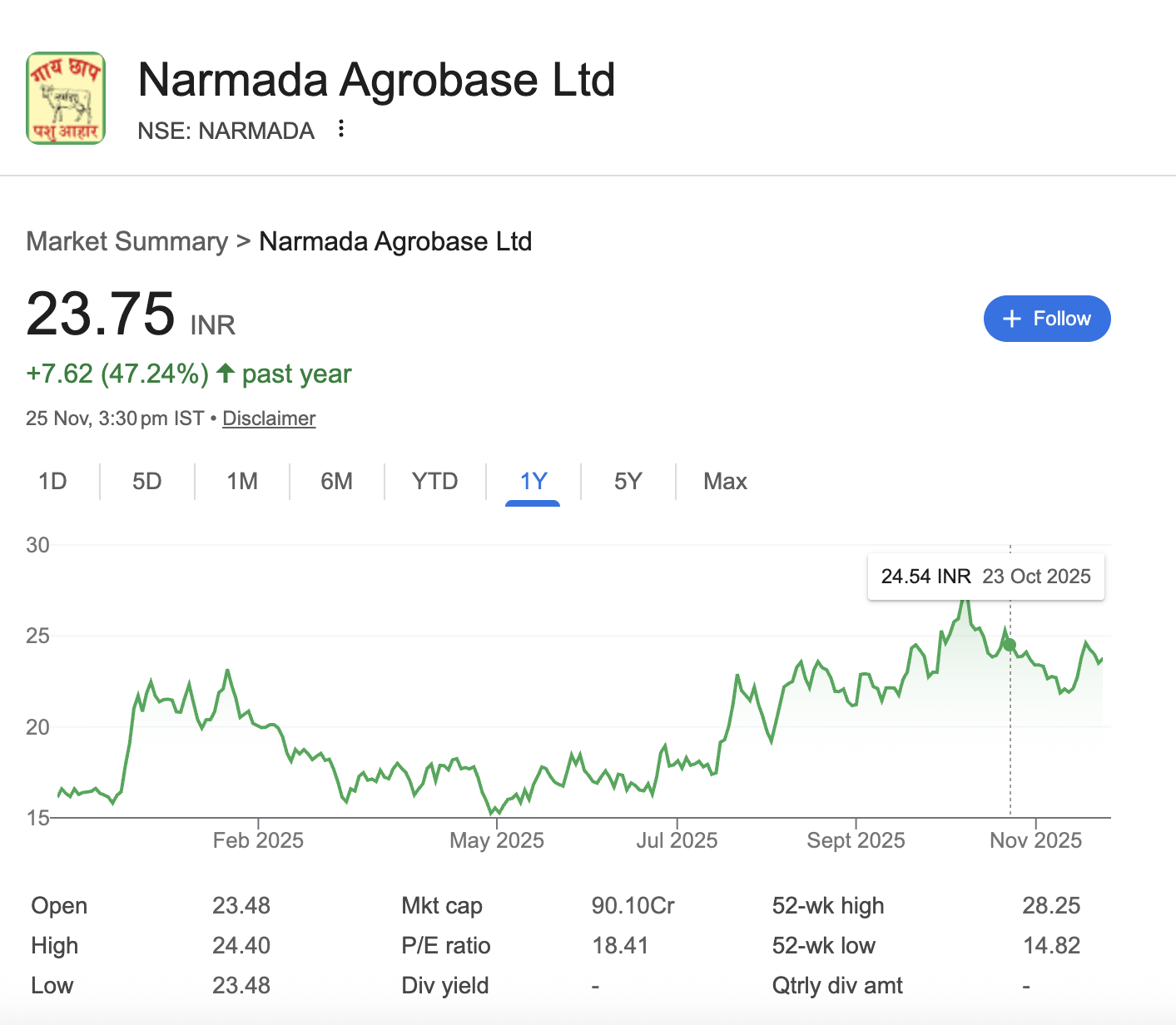

In the bustling ecosystem of Indian agro-processing, small-cap stocks often fly under the radar. But one Gujarat-based company, Narmada Agrobase Ltd. (NSE: NARMADA), is demanding attention with a financial performance that can only be described as explosive. From a 52-week low of ₹14.82, the stock has galloped to touch ₹28.25, rewarding investors with a staggering 47% return in the past year alone.

The question on every investor’s mind is: Is this a short-lived pump, or the beginning of a sustained growth story? A bottom-up analysis of its financials, operations, and market positioning reveals a company that is fundamentally transforming.

The Financial Engine: Dissecting the Growth Trajectory

At the heart of the buzz is a financial turnaround that is turning heads. The company has not only scaled up revenues but has dramatically improved its profitability, a key indicator of operational efficiency and pricing power.

The numbers tell a compelling story:

| Financial Snapshot (₹ in Lakhs) | FY23 | FY24 | FY25 | Growth (FY24-FY25) |

|---|---|---|---|---|

| Total Revenue | 5,002.60 | 5,032.07 | 6,567.66 | +30.5% |

| EBITDA | 201.83 | 251.76 | 557.57 | +121.5% |

| EBITDA Margin | 4.03% | 5.00% | 8.40% | +340 bps |

| Profit After Tax (PAT) | 65.22 | 101.94 | 408.80 | +301.0% |

| PAT Margin | 1.30% | 2.02% | 6.16% | +414 bps |

| Earnings Per Share (EPS – ₹) | 0.48 | 0.63 | 1.56 | +147.6% |

Source: Company Investor Presentation

This table isn’t just a collection of numbers; it’s a narrative of a company hitting its stride. The leap in PAT from ₹102 lakhs to ₹409 lakhs signifies that top-line growth is effectively trickling down to the bottom line. The expansion in EBITDA margin from 5% to 8.4% suggests better cost control and a strategic shift towards higher-margin products.

Beyond the P&L: A Strengthened Balance Sheet

The profitability surge has had a cascading effect on the company’s financial health.

- Net Worth has more than tripled, soaring from ₹169 lakhs in FY24 to ₹559 lakhs in FY25, providing a sturdy equity base for future expansion.

- The Debt-to-Equity ratio stands at a conservative 0.17, indicating low leverage and significant capacity to raise debt for Capex, if needed.

- Cash & Bank Balances witnessed a monumental inflow, increasing from ₹77 lakhs to over ₹1,480 lakhs, bolstering liquidity.

A note of caution for deep-value investors: the company reported a significant negative cash flow from operations in FY25 (-₹1,593 lakhs), primarily due to a sharp increase in inventory and trade receivables. This is a classic double-edged sword in high-growth companies—it can signal robust future sales or potential working capital challenges. Management’s ability to convert this into cash will be a critical metric to watch in the coming quarters.

The Bottom-Up Business: What Fuels This Growth?

Narmada Agrobase is not a speculative bet; its growth is anchored in a solid, dual-pronged business model.

- Cattle Feed (52% of Revenue): The company’s flagship brands, “Gasy Chhaap Narmada Pashu Aahar” and “Churma,” enjoy strong brand recall in the dairy-rich states of Gujarat, Rajasthan, and Madhya Pradesh. This segment benefits directly from India’s world-leading milk production.

- Cottonseed Products (48% of Revenue): The company processes cottonseed into oil cake (a high-protein cattle feed) and linters, which are used in the viscose, paper, and chemical industries. This diversifies its revenue streams and allows for a zero-waste operational model.

Key Growth Levers for the Future:

- Value-Added Products: The launch of pelletized cattle feed and molasses-enriched blocks commands higher margins and improves customer stickiness.

- Strategic Expansion: The company is actively expanding its dealer network into key markets like Maharashtra and Punjab-Haryana.

- Export Ambitions: Plans to tap into Southeast Asian, Middle Eastern, and African markets for both cattle feed and cottonseed products open up a substantial addressable market.

The Analyst’s View: To Invest or Not to Invest?

The Bull Case:

- Powerful Industry Tailwinds: The Indian animal feed market is projected to grow at a CAGR of 6.9% to reach INR 2,025 Billion by 2033. Narmada is a direct beneficiary.

- Operational Excellence: Its ISO-certified manufacturing, raw material pre-booking strategy, and buffer stock policy insulate it from commodity price volatility.

- Re-rating Potential: With a current P/E of around 18.41, the stock is not excessively priced for a company delivering triple-digit profit growth. A further expansion in multiples is possible if it consistently meets growth expectations.

The Caveats & Risks:

- Small-Cap Volatility: As a ~₹90 Cr market cap company, the stock is inherently more volatile and less liquid than large-caps.

- Working Capital Intensity: The recent surge in inventory and receivables needs to be monitored closely. Sustained negative operating cash flow is a red flag.

- Execution Risk: The ambitious expansion and export plans hinge on flawless execution, which is never guaranteed for a growing company.

The Final Verdict

Narmada Agrobase Ltd. presents a compelling case of a small-cap company transitioning from a stable agro-processor to a high-growth, profitable enterprise. Its financials for FY25 are undeniably strong, showcasing remarkable margin expansion and profit growth.

From an investor’s perspective, this stock is suited for those with a moderate to high-risk appetite seeking exposure to the burgeoning Indian agri-business sector. It is not a risk-free bet, but for those who believe in the management’s strategy and the company’s ability to manage its working capital, Narmada Agrobase offers a credible narrative of sustainable growth.

The company has planted the seeds; investors will be watching closely to see if the current harvest is a seasonal bounty or the new normal.

Disclaimer: “BrightStake” is only an Educational Platform and is not registered under any SEBI Regulations. All Information on this page is for Educational and Entertainment purposes only. Our content does not constitute any Trading or Investment advice. We make no representation of the Timeliness, Accuracy, Profitability, or Suitability of any share on this Website, and we cannot be held liable for any Irregularity or Inaccuracy. Our research is conducted solely for educational purposes, so please utilise our knowledge to inform your investment strategy.